Why do Gas Prices Change Constantly? - Understanding Price Elasticity

- Eshan Patel

- Jul 22

- 2 min read

What is Price Elasticity? (The basics)

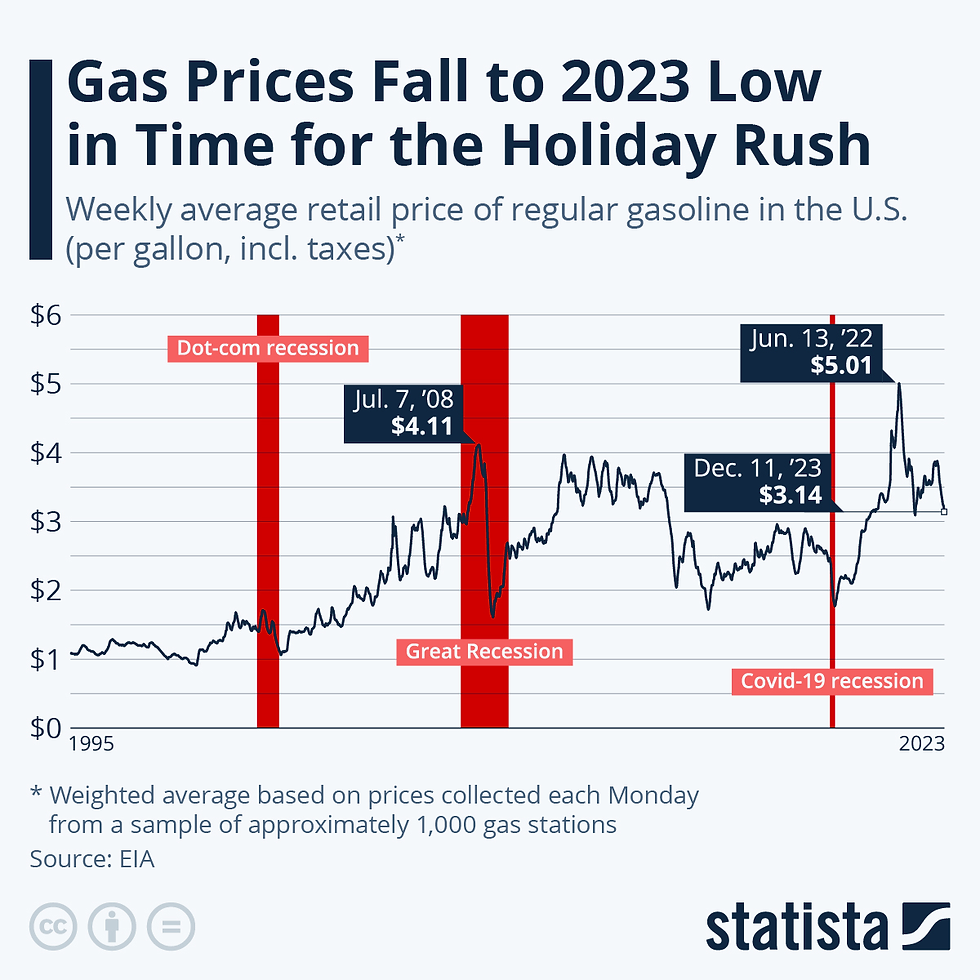

Imagine this. You are driving to school and you noticed that today, the gas price is $3.29 per gallon, but yesterday, it was only $3.10 per gallon. What’s going on? Why does the price of gas seem to change every time you pass the pump?To answer this, we need to talk about a key economic idea that doesn’t only affect gas, but essentially every item you use on a day-to-day basis: Price elasticity. Don’t worry, it’s actually WAY easier than it sounds.

So what is price elasticity, and how does it relate to gas prices? Price elasticity measures how sensitive people are to price changes for a product. If a product has elastic demand, people buy less if prices go up. For example, luxury cars. If a lamborghini shoots up to double in price than what it originally was, people are going to be a lot more hesitant to buy it.

On the other hand, if a product has inelastic demand, people buy nearly the same amount even if prices rise. This relates to gas! If gas goes from $3 to $6, people will still have to buy it no matter if it hurts their bank accounts or not because their cars can’t operate without it!

Why Gas Prices Fluctuate So Much

There are 3 main reasons why gas prices seem to always be changing. They are the changing prices of global oil, seasonal demand, and supply chain costs.

Global Oil Prices Changing: Gas prices are tied to Crude Oil, which is traded on global markets. Events like wars, natural disasters, or decisions made by OPEC (a group of major oil-producing countries) can disrupt supply and cause prices to rise or fall. For example, at the start of the Russia-Ukraine war, gas prices in America shot up to levels never seen before because Russia is a major crude oil supplier and their involvement in the war led to trade disruptions to America.

Seasonal Demand: Seasonal Demand plays a big role in price changes. Summer, for example, often brings road trips, vacations, etc, increasing need for gas, whereas demand typically dips in the winter. Gas stations and other gas suppliers will take advantage of this demand because they know gas has inelastic demand, meaning they can make a little bit more profit, and not lose demand for it.

Supply Chain Costs: Costs in the time between harvesting crude oil and turning it into usable gas into cars can lead to changes in gas prices. For example, if the harvesting materials or refining materials get harder to produce, that will slow the supply chain leading to gas prices shooting up. Or, if taxes go up in the countries where the crude oil is refined, then the companies will be forced to raise the prices for gas in order to counteract the taxes, leading to another raise in gas prices.

Conclusion

So next time you see gas prices jump overnight, you’ll know it’s not just random. It’s a mix of global oil markets, seasonal demand, and the inelastic nature of gas. Understanding price elasticity doesn’t make the price hurt less—but at least now you know why.

What’s your strategy when gas prices spike? Do you drive less, or just accept the pain at the pump?